You Say Yes, I Say No

You Say Yes, I Say No

NVDA Rips, Stocks Fall on Fedspeak

Let’s look at the facts. Powell has been trying to pivot since November. Internally, he must be getting pushback from the regional Fed Governors. I mean, how else do you explain Atlanta Fed President Bostic saying:

“Job growth has been great, which allows me to be more restrictive with policy.”

“Monetary policy has been less effective at slowing economic growth than in previous cycles.”

“The post pandemic economy may be less sensitive to Interest Rates.”

And I suppose that was the final push needed for the market to move a little more swiftly than just profit taking off the NVDA beat yesterday.

When it was over, equal weight SP 500 lost -2x the amount of the weighted index at (-143bps). The SPY/RSP Ratio closed at its highest level, 3.19, since Covid and is only 4% away from its highs registered in 2000.

Keep an eye on it.

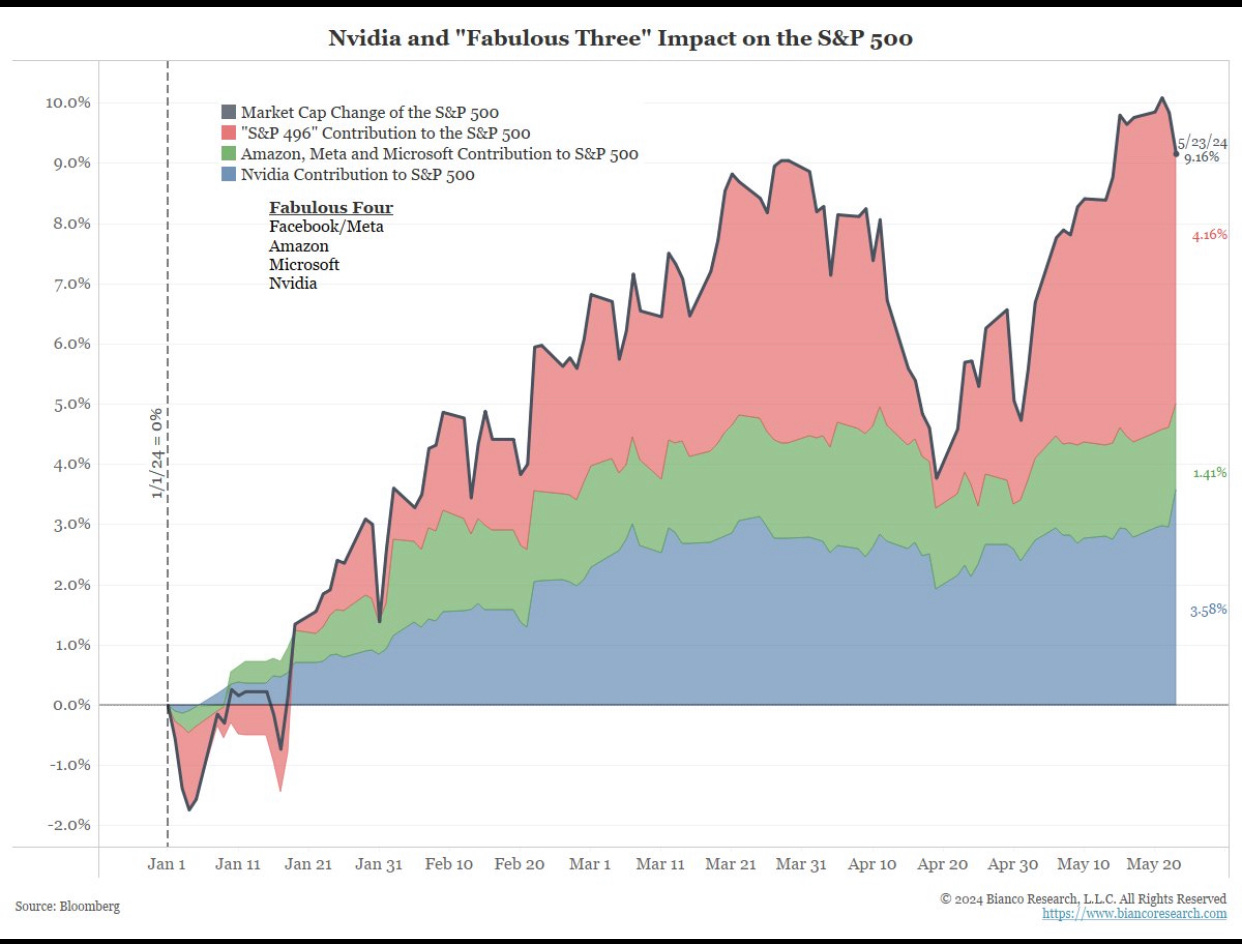

Jim Bianco out with an excellent post on the returns in the SPX year-to-date and how small the pool of participants actually is. This dovetails my equal weight Top50-Bottom50 from yesterday which had +1800bps of performance towards the Top 50 SPX stocks.

Take a look:

“The chart shows the change in the S&P 500's market capitalization, which is a good proxy for the returns calculated by S&P. This "simple" market capitalization change is up 9.16% YTD. 3.58% of this is gain NVDA. That's 39% of the S&P 500's gain YTD! AMZA, MSFT, and META account for another 1.41% of the S&P 500's gain YTD, or 15%. 54% of the S&P 500's gain YTD is just four stocks! These four stocks account for just 19% of the total market capitalization for the S&P 500.”

THOUGHTS

So, look, this is where we are at. Nation State Companies that are so big they exceed markets caps of the entire Energy sector, Canada, Germany etc. I mean, this is truly mind-blowing stuff. And in some ways, it feels as though we have become numb to the dislocation.

And that makes me wonder, maybe, just maybe this is going to spell opportunity. I mean, for those looking beyond the index trades themselves, the ability to create baskets and spread against other products has never been greater. I further suppose that the longer we press into Neverland, the more dislocation will occur. And just like in Banking with JPM and Hedge Funds (Citadel, Millenium etc) the NationState companies (AAPL, NVDA, AMZN, GOOGL, META) will continue to grow at the expense of the broader companies across the markets.

I mean, let’s not forget that the entire Russell 2k capitalization is less than a few of these stocks now. So, I wonder if these IWM, MDY type of products have become nothing more than short term trading vehicles?

And if that is the case, then a -160bps move on the back of NVDA and Rate’s staying higher for longer makes sense. I mean everybody has been pounding the table for a trade in IWM (me included, still long Straddles expiring at month end) and old Drunkenmiller supposedly puked his NVDA to buy a massive Call Option position in IWM. But then he also went out of business by missing the 1999-2000 ripper in Tech and then buying the top. Not a knock, just a fact that he has openly discussed. So, maybe he’s not great at cycle extensions in Techland?

I mean, who knows at this point, those scars were from 24 years ago and hell, 24 years ago I had dark hair.

My point is that this: We are in Huxley Land…Brave New World, Advanced Citizenship type of Game Theory in these single name issues. And it ain’t gonna stop.

At least not yet.

DAILY NOTES

On the road today, collecting the last of the brood for break, hence the brevity.

Yellen seems to have a pulse. Discussed openly the difficulties facing younger workers with food and shelter pricing this morning.

El-Erian with an Op-Ed in Bloomberg:

The combination of these three risks means that the current uniformity in Fed views, especially if maintained for more than a few months, risks unnecessarily undermining growth. A weakening of the most effective locomotive of global economic expansion would be accompanied by more pronounced currency and interest rate volatility, hitting over-indebted parts of the economy, such as commercial real estate, which are yet to be viably refinanced or have their assets disposed of in an orderly fashion.

I suspect that the question for monetary policy going forward is not whether the Fed will flip-flop again. Another U-turn is almost certainly in the cards for a central bank that continues to lack a strategic anchor, and that will react belatedly to growth slowing more than policymakers expect or are comfortable with. The critical question is whether this occurs in time to avoid significant economic and financial damage, particularly to the most vulnerable segments of the population.

Another first in the SP500. Never before had a stock with a <3% Weighting finished up more than 8% and the index close lower in a session.

GS adjusts its Rate Cut call. Now pushing it to September.

In the Journal of Environmental Psychology, a new study out with these findings:

The best place to relax is near water. After just 2 minutes of viewing water outdoors, blood pressure and heart rate drop. It's more calming to look at a lake, pool, or stream than trees or grass. Beaches are popular for a reason. Wider bodies of water bring more tranquility.

So hit the water this long weekend and Relax a bit!

Wine of the Week: Ratti Marcenasco 2018 Barolo (Italy). Get on the grill, cook some steak, smoke some meat and drink this wine!

Book of the Week: A Visit From The Goon Squad by Jennifer Egan.

Enjoy the weekend!