HiHo

Ah the American West. Conjuring up dreams of outlaws and expansion to the Pacific, the term “Wild” came into play during the Railroad Expansion (some would argue the Meme stocks of yesteryear). Well, shortly after the completion of World War 2, a TV show named the Lone Ranger was put on the airwaves and lasted for about 1300 episodes. Fighting Texas outlaws with perfect grammar, a strict moral code, an Indian sidekick and of course, his horse, named Silver. The Ranger personified good over evil and of course had his tag line, which is today’s title.

I thought about the Lone Ranger as I began to deep dive into the metals over the weekend. Silver up over 10% on the week. Copper up over 8%, Gold back to All-Time Highs, Uranium on the move…you get the picture. And so, it was time to conjure up some database work and see just how unusual some of these moves are and if in fact there is a continuing trade on the upside.

BAKE- “To overheat and overuse your horse. To ride him too long.” - Wild West Slang

The real question one has to ask themselves after such a rip rally in the metals sector is have I “baked” my horse? I mean, that’s trading. So, the question becomes is it time to take a rest, bring the horse to some water, and relax a bit before saddling up again? Let’s take a look.

SILVER

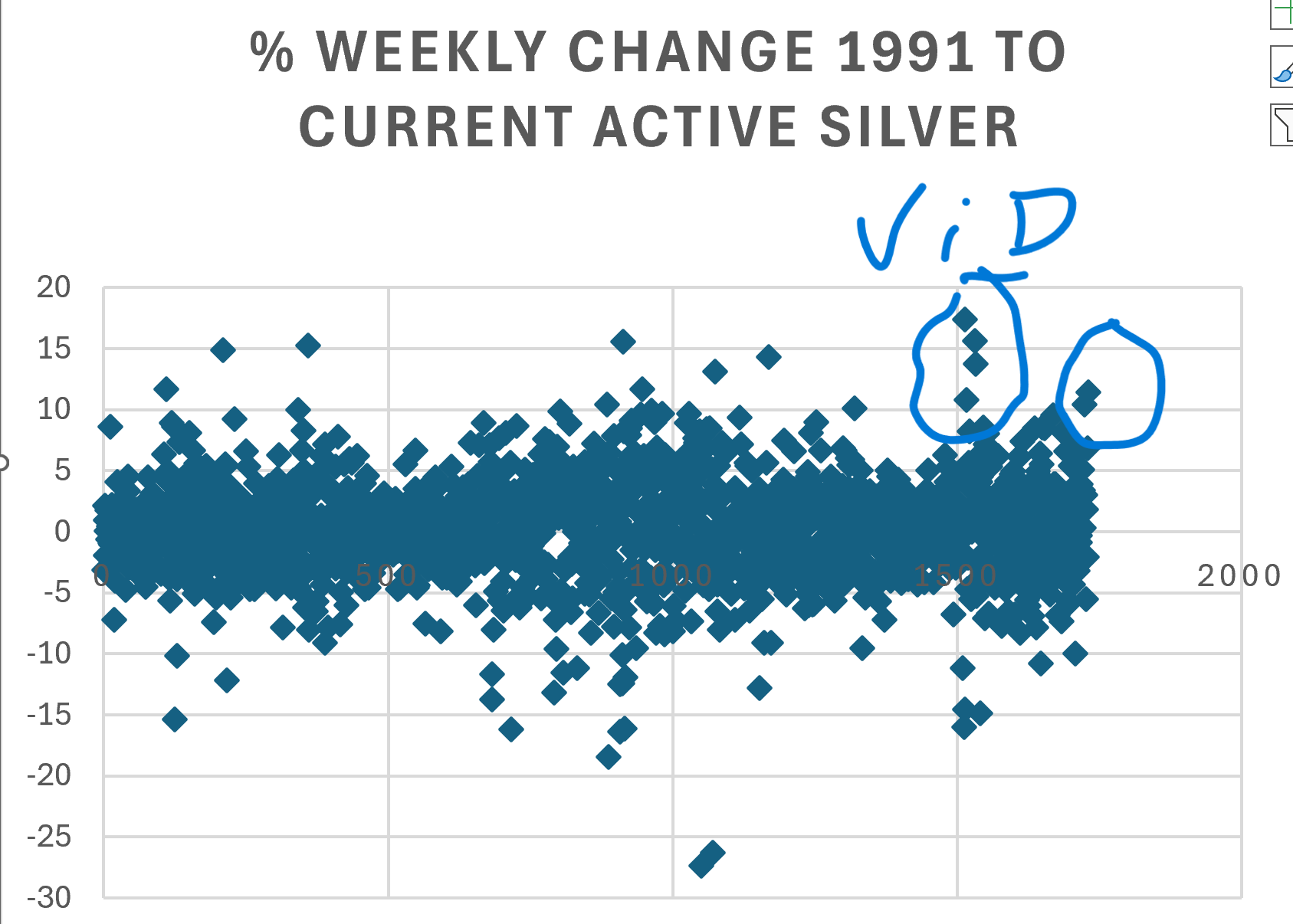

Going back to 1991, Silver has had <10% weeks 15 times, including last week (point of technicality, I measured the futures close on Friday to the SLV ETF 4pm EST close, not the 1:30 EST Futures close).

Technically, this is a Standard 3 Deviation Event. There is a 0.84% chance that the Silver market moves 10% or more in a week since 1991.

So, this clearly qualifies as an event, let’s break it down:

As you can see from above, it is a rare week that Silver moves like this. Take away Covid and the odds would go lower as 4 of the occurrences happened around that event.

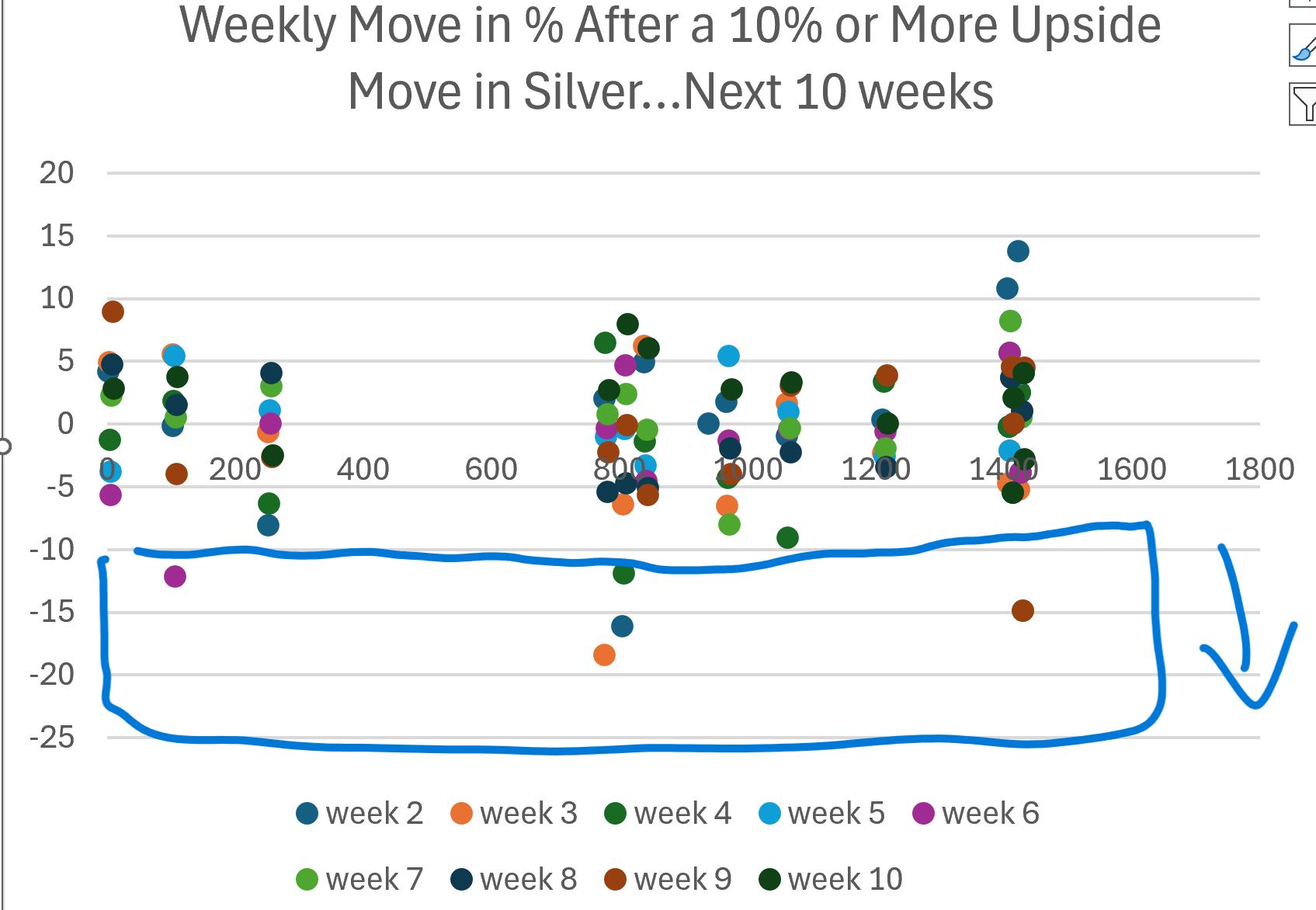

The following chart represents each of the 10 weeks post Event (<10%) in % terms of return in Silver.

As you can see from the above returns, the risk of downside large moves are prevalent. Most of the week’s hover between +/-5% and only our current episode (far right) has added +10% moves in the same measurement period (Silver rallied +10% 6 weeks ago as well).

So, that is a new piece of info (consecutive events within a certain time period).

The other key piece of info here is that last week’s event of <10% is the only event in our measurement where Silver closed above a 3 year high.

The question that leads me to ask, is this: Is Silver Baked?

I mean, ultimately, that is hard to know. But what the data above shows is that after a <10% move, the contracts tend to get volatile. This is not a sell signal; it is a volatility signal.

Accordingly, if one is a little anxious and wants to bring the horse to water while still maintaining their respective long position, it might be time to sell some upside calls for a couple of weeks against your longs.

Let the dust settle, enjoy a drink, collect some premium and wait for June is my play.

COPPER

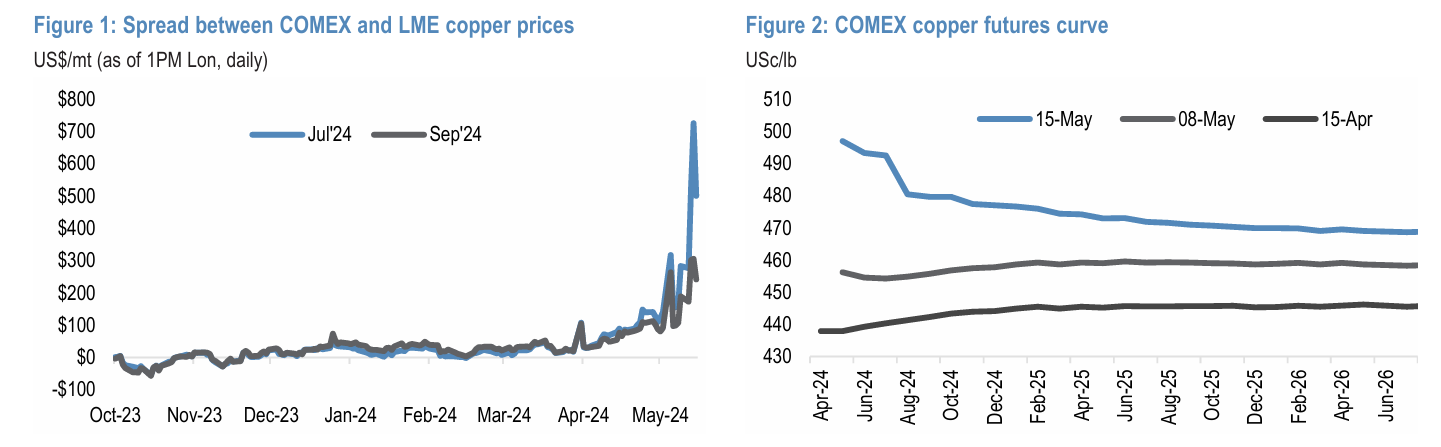

Copper ripped to a record close on Friday. But underlying the move is some very technical action between the ARB in London and NYC. The spread broke it’s normal decades old correlation and clearly caught some players offsides, which led to the price spike.

Here is a recap:

The massive widening of the COMEX/LME copper arb is more about positioning and supply/inventory tightness in the US specifically and the ability and timing to unwind it given limitations on COMEX deliverability.

We do not think it is reflective of a tight broader global refined copper market, which still appears quite loose at the moment, particularly in China.

We remain structurally medium-term bullish on copper prices over the next two years with an upside target of $11,500/mt in 2025 but current price levels are running ahead of our forecast and well ahead of global refined market fundamentals at the moment.

Constrained mine supply in copper is not going to alleviate quickly, which still leaves us on the cusp of significant refined market tightening in the coming quarters in our view.

Though the feed down from tight upstream concentrate markets to physical shortages in refined copper markets is taking longer to play out, in large part due to resilient Chinese refined copper supply and more acute weakness in Chinese purchasing over the last two months.

We still think Chinese copper demand is being deferred and delayed in the face of rising prices at the moment, rather than outright destroyed.

Given significant financial length in copper and persisting slack Chinese fundamentals for the time being, we think there remains the risk that investors lose some patience with the story and take profit more widely, driving a temporary correction lower in prices over the coming weeks and months.

In our view, this could ultimately be a very healthy correction that acts to kick start Chinese demand out of its stupor, beginning to finally take slack out of the market.

It would also likely lay the groundwork for another eventual push even higher in prices as refined fundamentals begin to catch up to prices at a time when refined copper supply risks continue to intensify later this year and into 2025.

So, let’s get technical on the situation:

The copper market was stunned this week as the premium of Jul24 COMEX copper over the equivalent LME contract widened massively to more than $1,000/ mt intraday on Wednesday as the COMEX curve flipped into steep backwardation.

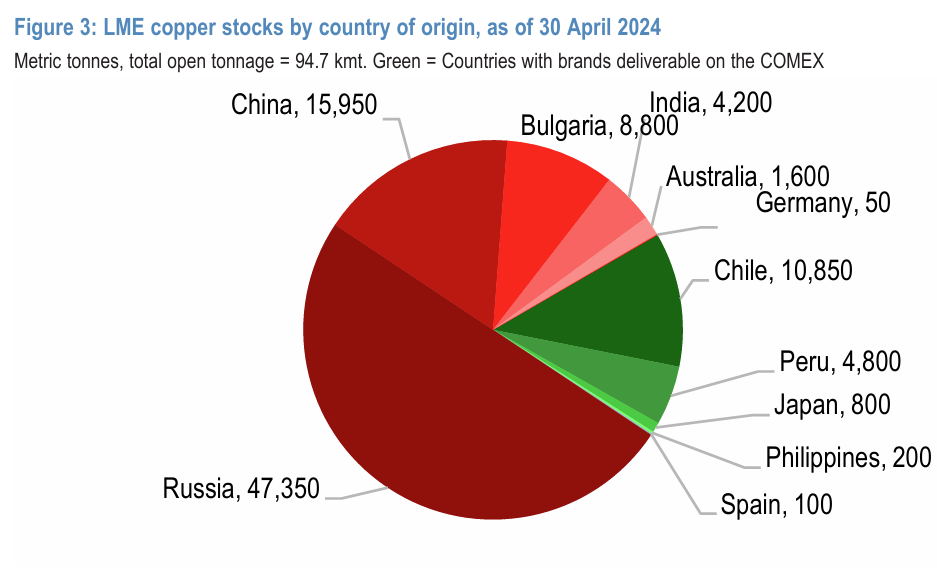

Amid solid demand and weaker imports to start the year, visible copper stocks in the US are tight with under 19 kmt sitting in COMEX warehouses (down from around 28 kmt at their 2024 ytd peak in late March) and inventory in US LME sheds drawing to only around 8 kmt this week, down from a peak last November of nearly 100 kmt.

This lack of immediately available metal to deliver into the COMEX contract set the groundwork for this week’s squeeze. Amid a wait for physical arrivals of copper eligible for COMEX delivery to close the arb, holders of COMEX shorts (market participants positioned for a normalization in the arb via a short COMEX/long LME trade and/or with the ultimate aim to eventually deliver into COMEX shorts) were pressured to either roll forward or close the trade amid escalating losses and margin calls.

This dynamic, along with the sizeable systematic length built on COMEX but unlikely to roll until later, drove the illiquid spike in COMEX prices and spreads.

Fundamentally, we are now in a waiting period for additional copper shipments to arrive to the US, with COMEX deliverable shipments from South America in particular focus. Anecdotal reports are emerging that copper producers and traders are now in the process of shipping more metal to the US to profit from the arb.

This reportedly includes Codelco (COMEX deliverable) which, according to Bloomberg reporting, is directing all available shipment volumes to the US and also negotiating to postpone existing sales to other customers to maximize US deliveries.

Separately, FastMarkets reports that copper fabricators in China and Southeast Asia are also now asking for a postponement of copper cathode shipments under long-term contracts, given a let up in demand.

This could potentially allow for a more smooth diversion of previously contracted volumes headed to Asia to be diverted towards the US too. Prior to this week, reports also surfaced that Chinese smelters plan to export ~50 kmt of copper to LME warehouses in Asia, though no Chinese brands are directly deliverable onto the COMEX exchange.

Even if not brand eligible, additional copper imports into the US (whether from China or other countries) could theoretically be swapped for COMEX deliverable metal heading to US consumers to close the arb and replenish stocks.

The copper market experienced a similar episode of a widening in the COMEX/ LME arb in June & July 2021, albeit not to the same extremes as the current episode. At that time, US copper cathode imports rose from an average of around 60 kmt per month over the twelve months through July 2021 to an average of 96 kmt per month over August, September and October 2021.

These boosted inflows allowed for an eventual replenishment of COMEX stocks and a normalization of the arb. For reference, in 1Q24, the US imported around 180 kmt of refined copper cathode, down by ~15% yoy, with ~70% of imports coming from Chile (Figure 5 U S re f in ed copp er ca th od e im p o r ts b y o r ig in ). For its part, China took around 200 kmt of refined copper imports from Chile in 1Q24, with February and March coming in around 60 kmt per month.

THOUGHTS

I mean, this is pretty technical stuff and it certainly is a well structured read through on what has happened and somewhat predictive on what could happen. And, just like with Silver, the question becomes has Copper been baked?

As you know, I exited my final position in the runup last week and have no dog in the fight. I will admit that while I was aware of the ARB issue, I did not pay it great mind. Ultimately, this squeeze was a clear generator of price. So, the only real question facing the market is this:

Is the ARB squeeze over?

If yes, I would expect Copper to move a few % lower and build a base area before the next leg (that leg could be higher or lower).

If no, I would expect another squeeze in the front month and the backwardation of the curve to continue and press hard into July Contract expirations.

Keep an eye on it.

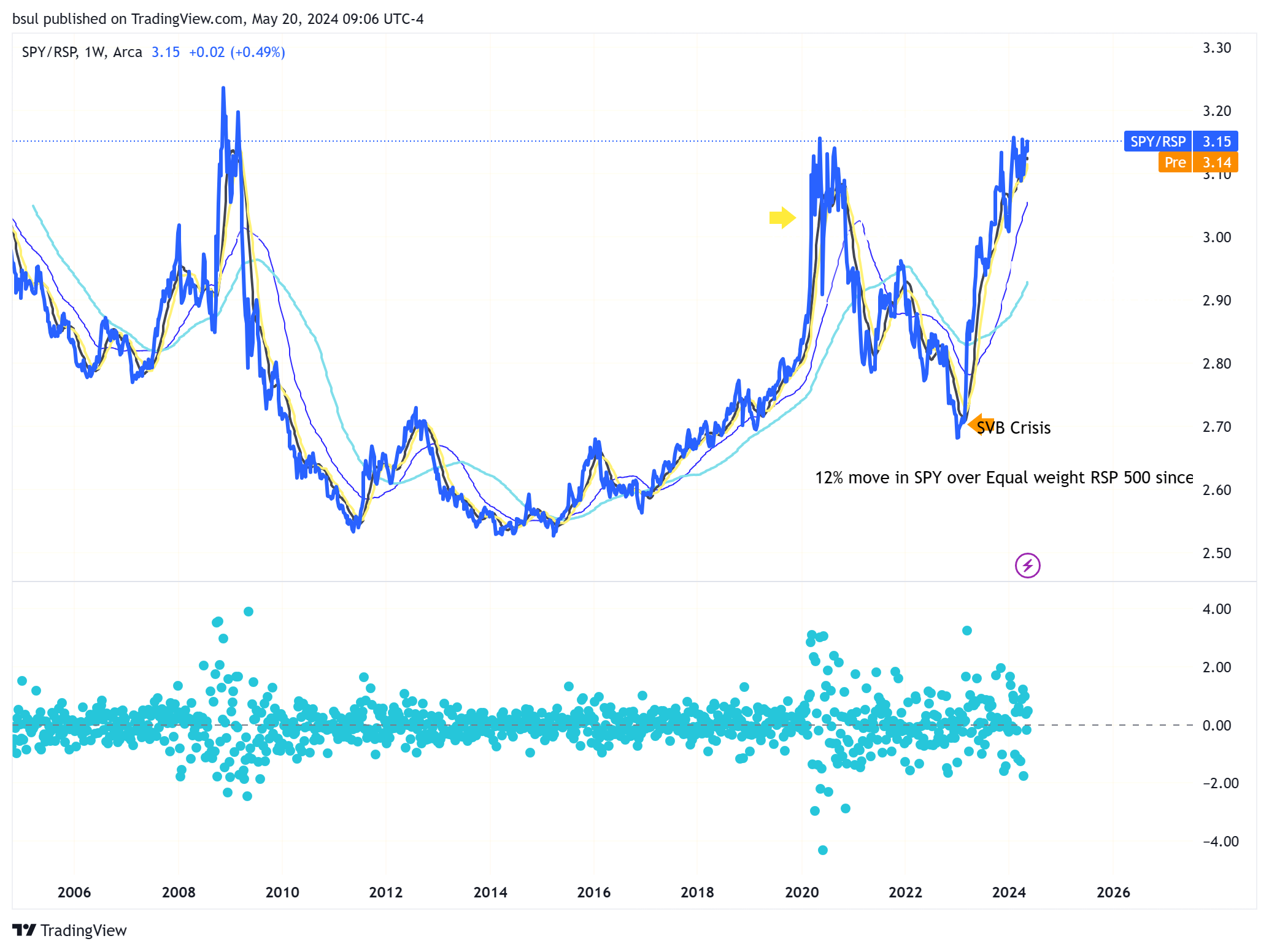

SP 500 Weighted Vs Equal Weight (SPY/RSP)

I’ve discussed this spread for several months. We closed the week at 3.15 in the Ratio, essentially at the highs of this move and bumping up against resistance from last year’s high zone.

Q4 ‘23 undid the highs as bets were made on broadening the market and the undoing of the concentration of the Mag7. But as rates ticked back up, so did the Ratio. And now we are at relative highs with a big event on Wednesday. And that event is NVDA earnings.

NVDA is the 3rd largest holding in the SPX at 5.12% of the index. It stands to reason that a beat and guide could propel not only the stock but this Ratio and further cement the concept that bigger is better…at least when it comes to stocks.

Note the chart below and keep an eye on it.

DAILY NOTES

Iranian President Raisi is confirmed dead in a helicopter crash.

NYT with a piece on how high rates have not ravaged the economy as many feared. But the consequence on middle to low-income earners has been dire as many have maxed out credit and are now falling behind in payments.

Yardeni tripling down on his “Roaring 20’s” thesis. See’s 50% gains possible by 2030 in the DOW and SPX.

Et Tu Brute?

MS Strategist Wilson turns away from the Bear Side:

Morgan Stanley’s Michael Wilson now sees the S&P 500 rising 2% by June 2025, a major about turn from his view that the benchmark will tumble 15% by December.

The strategist — whose bearish 2023 outlook failed to materialize as markets kept rallying — finally gave in and boosted his target for the S&P 500 to 5,400 points from 4,500. That catapults his forecast from among the lowest on Wall Street to one that projects a fresh record for the index.

“In the US, we forecast robust EPS growth alongside modest multiple compression,” Wilson wrote in a note on Sunday with his Morgan Stanley colleagues, as they discussed the firm’s second-half views across various assets.

Generally, the bank expects a “sunny macro environment,” which will support risk assets in the second half of the year, although Wilson reiterated his view that broader outcomes for the economy are becoming hard to predict as data become more volatile.

The Morgan Stanley strategist recommends a barbell approach of quality cyclicals stocks and quality growth and maintains a long exposure to certain defensive areas such as consumer staples and utilities.

And then there was 1: Marko and the Boys:

Wilson’s 20% upgrade leaves JPMorgan Chase & Co.’s Dubravko Lakos-Bujas among the few remaining prominent bears on Wall Street. His forecast calls for a slump of more than 20% in the S&P 500 by year end.

Lakos-Bujas’s colleague, Mislav Matejka, said Sunday that US earnings are unlikely to jump sharply in the third and fourth quarters to meet the current consensus if economic data remain weak.

BofA’s Hartnett out trying to find some reason’s to get long the 30yr. Come’s up with this: 55% of his survey respondents think policy is too stimulative. A combo of easier Monetary Policy and Tighter Fiscal Policy could lead to supportive environment for the long end.

I suppose that with everyone bullish, and the VIX on it’s knees, it would be time to think about shorting the market. But I tend to think the better play is to wait and see if this rally can get stupid and outlier. If that were to occur, well then we would have ourselves a great Asymmetric setup around Q4 into Q1 ‘25.

Trade Em Well Today